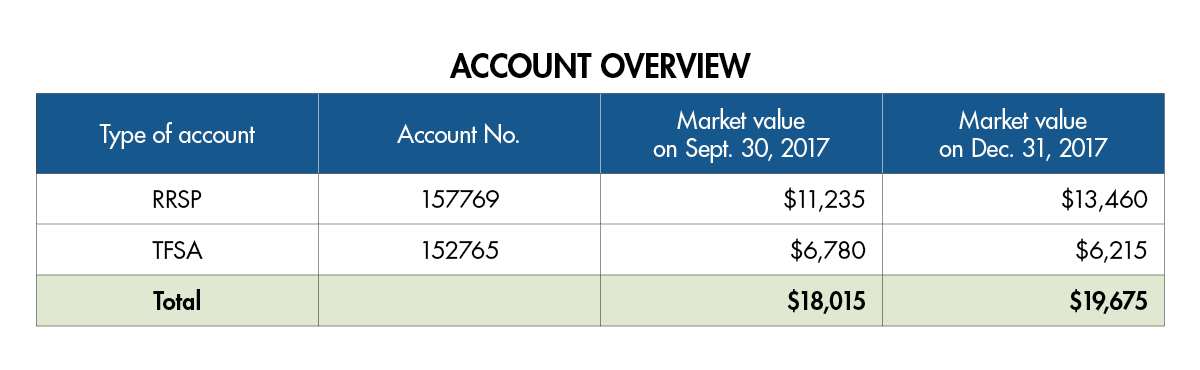

Do you have investments, such as shares, bonds or mutual funds? If so, you receive an investment account statement listing your investments. It is usually issued every three months by the firm you deal with. This essential tool is a source of information that details:

- The total marketAn exchange, such as a stock exchange, is a market where investors can buy and sell securities, including shares and options.

In order for a company to be listed on an exchange, it must meet certain criteria and regulations, relating to accounting practices and information for shareholders, for example. value of your investments - Changes in and returnA return is the gain you earn on your investment in the form of interest income, dividends, or capital gains.

The return is often calculated as a percentage. If an investment of $1,000 earns $20 per year, then the rate of return is 2% ($20 / $1,000 = 2%). on your portfolio - The breakdown of your investments according to assetThe assets of a person or a company are everything that belongs to them. These assets may be tangible (such as a computer or a building) or intangible (such as patents, trademarks or copyrights).

Assets are the opposite of liabilities, which represent the debts of the person or company. class

Just as you would check your bank account statement or pay stub, it’s a good idea to review your investment statement to check for changes in your portfolio.

When you receive your statement, take a few moments to review the transactions. If any of them seem questionable, don’t hesitate to contact your representative for answers.

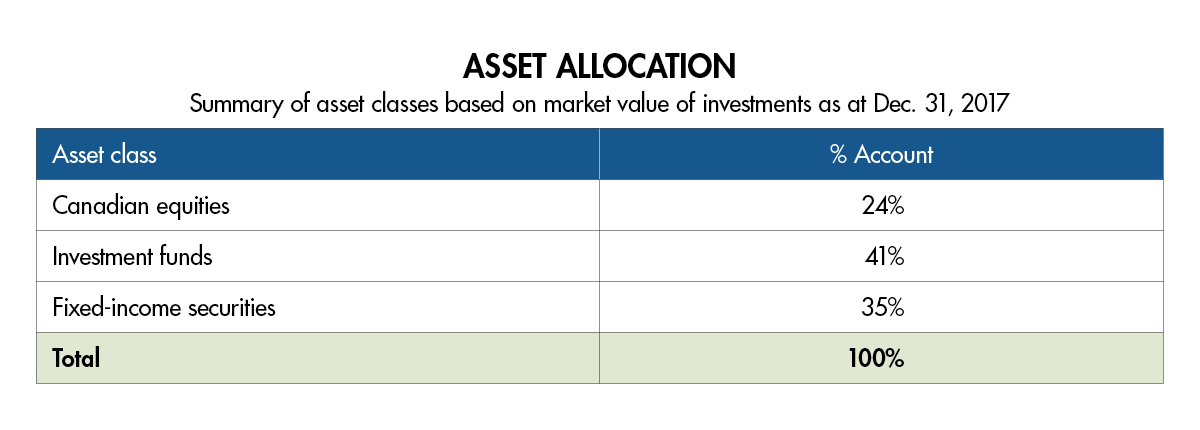

The statement also provides information about the allocation of your assetsThe assets of a person or a company are everything that belongs to them. These assets may be tangible (such as a computer or a building) or intangible (such as patents, trademarks or copyrights).

Assets are the opposite of liabilities, which represent the debts of the person or company. based on market value. The allocation is indicated, for example, by the percentage of money market securitiesUn actif financier émis notamment par une société ou un état qui confère des droits dans une entreprise ou dans une créance et qui peut être vendu ou acheté.

Voici des exemples de titres :

un bon du Trésorun certificat de placement garanti (CPG)une obligation d'épargneune actionetc., mutual fundsUn fonds commun de placement (FCP), ou organisme de placement collectif, est le regroupement de l'argent de plusieurs investisseurs, qu'un gestionnaire utilise pour acquérir des actions, des obligations ou d'autres titres en fonction des objectifs du fonds. or sharesA share, also referred to as stock, is an equity security that entitles you to an ownership interest in a company.

The company can distribute a portion of its earnings to shareholders by paying them a dividend.

The shares of companies listed on an exchange are bought and sold at the exchange.

When a company ceases to operate, the proceeds from the sale of its assets are used to pay its debts and taxes, and the rest of the money is distributed to shareholders. you hold.

Make sure the information on your statement reflects your investor profile ![]() This link will open in a new window and your objectives.

This link will open in a new window and your objectives.

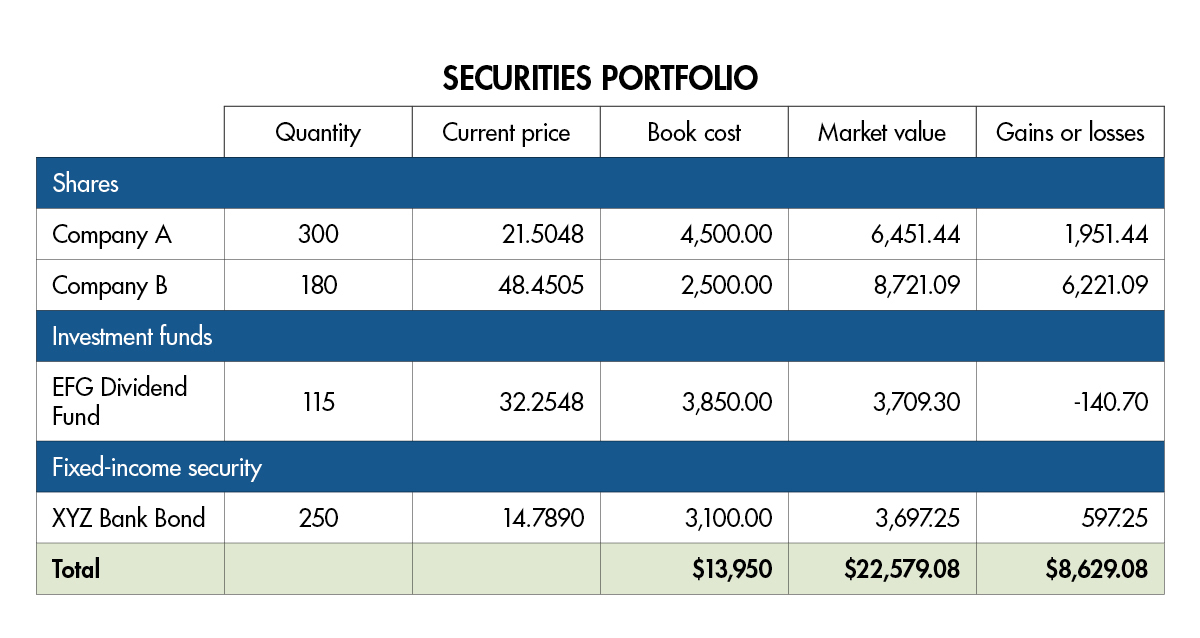

There is also a list of your investments and, in most cases, their book cost and market value.

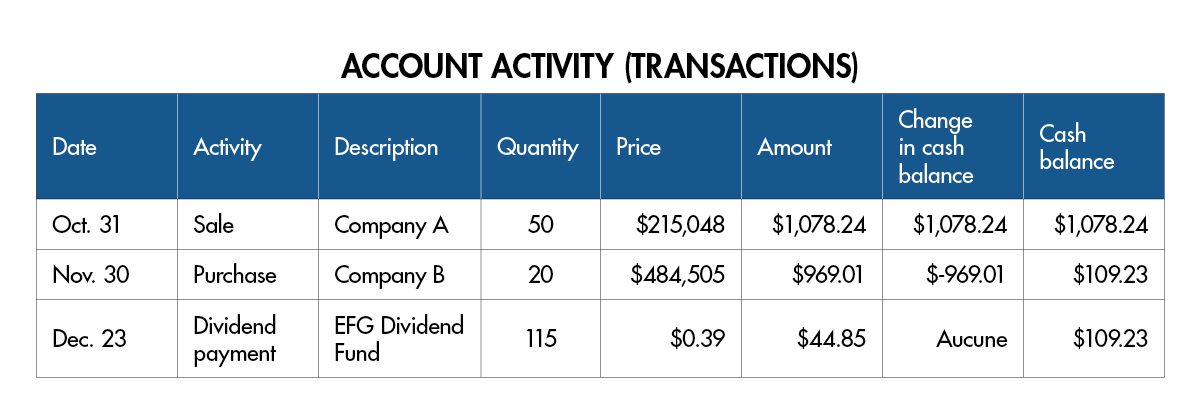

The investment statement outlines transactions carried out in your account during the period: sales, purchases, dividend payments, reinvestments, etc.

When you receive your statement, take a few moments to review the transactions. If any of them seem questionable, don’t hesitate to contact your representative for answers.

The statement also provides information about the allocation of your assetsThe assets of a person or a company are everything that belongs to them. These assets may be tangible (such as a computer or a building) or intangible (such as patents, trademarks or copyrights).

Assets are the opposite of liabilities, which represent the debts of the person or company. based on market value. The allocation is indicated, for example, by the percentage of money market securitiesUn actif financier émis notamment par une société ou un état qui confère des droits dans une entreprise ou dans une créance et qui peut être vendu ou acheté.

Voici des exemples de titres :

un bon du Trésorun certificat de placement garanti (CPG)une obligation d'épargneune actionetc., mutual fundsUn fonds commun de placement (FCP), ou organisme de placement collectif, est le regroupement de l'argent de plusieurs investisseurs, qu'un gestionnaire utilise pour acquérir des actions, des obligations ou d'autres titres en fonction des objectifs du fonds. or sharesA share, also referred to as stock, is an equity security that entitles you to an ownership interest in a company.

The company can distribute a portion of its earnings to shareholders by paying them a dividend.

The shares of companies listed on an exchange are bought and sold at the exchange.

When a company ceases to operate, the proceeds from the sale of its assets are used to pay its debts and taxes, and the rest of the money is distributed to shareholders. you hold.

Make sure the information on your statement reflects your investor profile ![]() This link will open in a new window and your objectives.

This link will open in a new window and your objectives.

There is also a list of your investments and, in most cases, their book cost and market value.

The investment statement outlines transactions carried out in your account during the period: sales, purchases, dividend payments, reinvestments, etc.

Book cost and market value

Most investment account statements provide information about the book cost and market value of investments.

The book cost, or book value, is the total amount paid to purchase an investment, including any transaction charges. The amount is adjusted to reflect reinvested distributions, among other things. For example, rather than cashing out the earnings realized, you can reinvest them automatically to purchase other shares.

Market value is the actual value of an investment security on the markets at a given date. This is the amount you would obtain if you sold your investment on that date.

If the market value is higher than the book cost, you make a make profit.

Two reports to clarify your investments

The investment account statement informs you about changes in your investments, but it can be difficult to get a more general overview of their performance. For example, do you know your personal rate of return? Does your statement show the charges and compensation you pay for various services and advice?

To help you see where you stand, you will receive two annual reports:

- Investment performance report

- Service and charge report

These reports contain detailed information about your account’s performance and the charges that you pay the dealer or adviser you do business with.

Understanding your investments better

The new reports are designed to support investors’ understanding and knowledge of investing so they can make informed decisions.

The reports stem from the rules under CRM2 (Client Relationship Model Phase 2) requiring investors to receive clearer information.

Whether you are investing for your retirement or to help pay for your children’s education, knowing your investments’ performance will help determine if your portfolio will allow you to achieve your goals.

The annual investment performance report provides information about the overall performance of your investments as well as changes in the value of your account (in dollars) and its performance (as a percentage) during the year.

You will see how different investments have evolved. It also provides you with your personal rate of return, which tells you how your account has performed over the past year and since it was opened.

This single rate is calculated using the money-weighted rate of return. It is based on cash flows in your account (deposits, withdrawals, earnings, etc.) and changes in the market value of the investments held in your account.

As time goes on, this report will include your personal rate of return for the past 3, 5 and 10 years.

Difference between time-weighted and money-weighted rate of return

Anoko and Denis invest in the same mutual fund. The first year, Anoko invests $5,000 and Denis invests $1,000. At the end of the year, the fund posts a return of 14%.

At the start of the second year, Anoko invests $1,000 in the fund and Denis invests $5,000. However, the fund loses 6% of its value compared to the previous year.

| Time and weighted rate of return | Anoko | Denis | Fund performance |

|---|---|---|---|

Year 1 | $5,000 | $1,000 | 14% |

Year 2 | $1 000 | $5,000 | -6% |

Time-weighted rate of return at end of year | 3,52% | 3,52% | n/a |

Money-weighted rate of return (personal annual rate of return) at end of year 2 | 2,7% | -3,3% | n/a |

The time-weighted rate of return for both investors, which may appear in advertising for the fund, is the same at the end of year 2, namely, an annual return of 3.52% (cumulative return of 7.2%). The time-weighted rate of return takes only fund performance into account, not the impact of investor deposits and withdrawals.

As for the money-weighted rate of return (personal annual rate of return), it is not the same for Anoko (2.7%) and Denis (-3.3%) because Anoko invested more money than Denis when the fund was performing well.

2- Annual report on charges and other compensation

The fees you pay reduce your returns. It’s important to understand the impact of fees and expenses on your return.

The report on charges and other compensation indicates the amounts collected by the firm from which you received services and advice in the past year, including:

- Trailing commissions

- Administration fees

- Transaction fees

- Deferred sales charges

- Fees

The report does not provide information about the representative’s personal remuneration, but only that of the firm you deal with and that employs him. For more information, contact the firm you do business with and consult the documentation for the products you hold.

For more information, contact the firm you do business with and consult the documentation for the products you hold.